Are you properly addressing working capital in your purchase agreement?

By Christopher Hewitt

Almost every M&A transaction includes some form of working capital true-up, and yet many practitioners, including attorneys, accountants, and business development professionals, seem to struggle with this provision. In this series of posts, I will discuss my perspective on the objective the working capital true-up should attempt to accomplish, and identify and explain some of the most common problems that I have seen in my practice with this provision. This first installment will address the purpose of working capital and how that purpose relates, if at all, to target working capital in a transaction. In future posts, I will examine some of the issues in the mechanics of a working capital true-up, rollover equity and the working capital true-up, and the idea of a “cash-free” business and working capital.

The Purpose of Working Capital

I think I can safely say that everyone who has encountered a working capital provision at least once knows that the accounting definition of working capital is current assets minus current liabilities. For many practitioners, however, that is where the attempt to understand working capital begins and ends.

Working capital represents the operating liquidity available to the business. Stated differently, it is the amount of capital required by an organization to meet its day to day expenses without the infusion of outside capital.

Working capital management is one of the most important issues facing an organization. Organizations can reduce their financing costs, increase the funds available to expand the business, or increase the return to shareholders by effectively managing working capital. To the extent that management is able to generate cash that exceeds the amount required to operate the business on a daily basis, it can use those excess proceeds to pay down debt, invest in the business, return excess funds to shareholders, or some combination thereof.

Similarly, the purpose of requiring that a certain amount of working capital be left in an acquired business should be to make sure that working capital is sufficient for the buyer to operate the business post-closing so that it need not inject cash into the business. Stated differently, the current assets purchased by the buyer—e.g., inventory, accounts receivable, prepaid expenses, and, yes, even cash—should be sufficient to pay off the current liabilities assumed by the buyer—e.g., accounts payable—as well as to produce more inventory, make payroll, and pay other daily expenses of the business.

Target Working Capital

With this backdrop in mind, the first critical issue to consider in the working capital true-up is the amount of working capital necessary to accomplish the foregoing objective—called the target working capital.

Probably the most common method parties use to calculate target working capital is the trailing twelve month (TTM) average of the actual working capital of the business being acquired, adjusted for items the buyer is not taking, e.g.,the current portion of long-term debt and taxes. While this approach may have appeal in its simplicity, it completely fails to consider the purpose of working capital as discussed above. It also fails to consider how the parties arrived at the headline purchase price, whether or not the business is growing, or seasonal fluctuations in working capital.

If the purpose of working capital is to pay the day-to-day expenses of the business, the business generates more cash than is necessary to run the business, and the seller neither reinvests that extra cash nor distributes it to shareholders, one can see how the TTM average would overstate required target working capital. This scenario is actually very common in privately held companies where the shareholders are not concerned about managing working capital or taking money out of the business.

Conversely, if the business does not generate enough working capital to fund the daily operations of the business, and the business needs to borrow or receive an equity infusion, the TTM average would understate what should be the target working capital. Thus, an analysis of the amount of cash it actually takes to operate the business, and not calculating some mathematical average, is the effort that should be put forth to determine the target working capital. Admittedly, this could be a difficult task in many situations, especially where a seller is trying to convince a buyer to pay seller for the working capital in excess of “normalized” working capital.

Another aspect to consider is how the parties, or at least the buyer, arrived at the purchase price. If the buyer based its purchase price on historical earnings or EBITDA, then looking at an historical average of working capital may work. Even it that case, however, the parties should look to see what working capital is necessary to operate the business as the seller operated the business over the preceding periods. It would be coincidental at best if this amount were the TTM average.

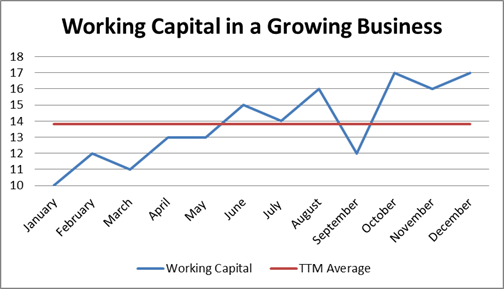

Conversely, if the business sold is growing and the buyer paid for that growth, i.e., the prospects of the business, then the target working capital should be the amount necessary to run the business as anticipated to be run to generate that growth. In this situation, a TTM average will in all likelihood be below the amount of working capital necessary to generate the growth paid for. The following graph highlights how the TTM average would significantly understate required working capital in a growing business, assuming a December 31st closing date. In this case the buyer would be paying the seller for the “extra” working capital, which is really necessary to operate the growing business.

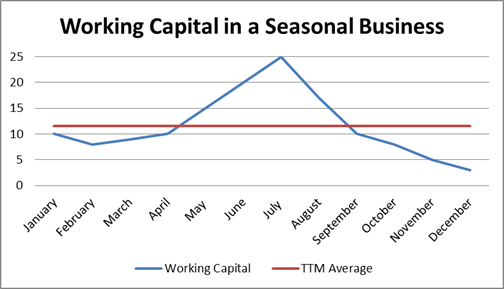

Similarly, in a business with seasonal fluctuations in working capital, using the TTM average may either understate or overstate target working capital depending on when during the year the business is acquired. As depicted in the following graph, assuming each year looks similar, using the TTM average results in an increase or decrease in the amount paid at closing based simply on when the business is acquired due to seasonality. While there is an argument to be made here that the TTM average smoothes out seasonality, I think it would again be purely coincidental if the TTM average equaled the true working capital requirements of the business.

As part of the financial due diligence, the parties and their advisors should strive to understand the working capital necessary to operate the acquired business, as it is currently run or is anticipated to be run, in determining the purchase price. Otherwise, the seller could be leaving money on the table in the form of excess returns that it had not previously paid to itself, or the buyer may not be receiving the full value of its purchase price in that it may need to inject capital into the business shortly after acquiring it.

In the next post, I will examine the mechanics of the working capital true-up and discuss why the parties to a transaction should not consider the working capital adjustment as purchase price.